Indian Crypto Traffic Took a Nosedive as Tax Regime Tightened

Indians have lost interest in trading on local crypto exchanges since the government began imposing taxes on profits and transactions, data from AppTweak and SimilarWeb shows.

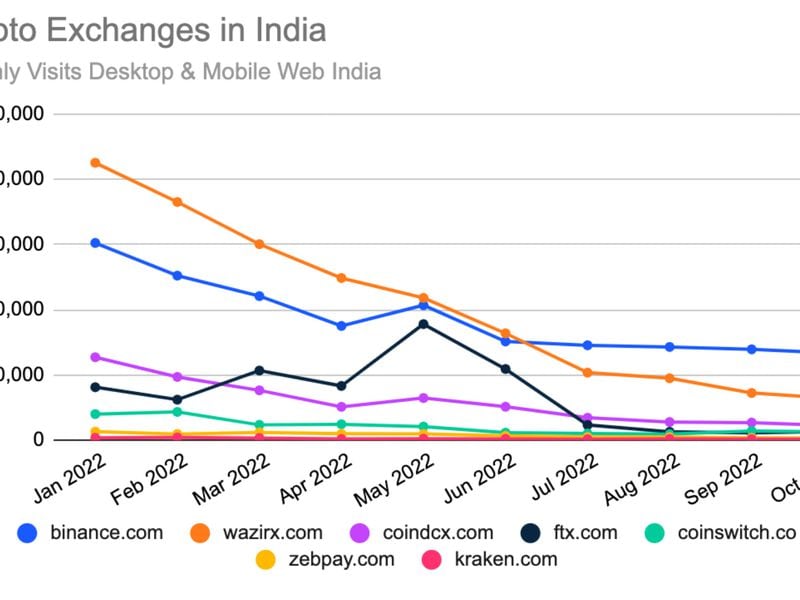

However, interest in Binance, the world's largest exchange by trading volume, has remained more or less constant. The exchange is not based in India and thus is not subject to its jurisdiction, even if its users are.

Visits to Indian exchanges Wazir X, CoinDCX, CoinSwitch Kuber and ZebPay fell 80% between Feb. 1 – when Prime Minister Narendra Modi’s government announced a 30% tax on crypto profits and a 1% tax deducted at source (TDS) on all transactions – and Oct. 31, according to SimilarWeb. App downloads fell 93%, AppTweak shows.

The tax on crypto gains kicked in starting April 1 and was set at the same level as taxes on earnings from online casinos. But the industry was hit harder by the second tax, which took effect July 1 and was aimed “more for tracking transactions,” Indian Finance Minister Nirmala Sitharaman said.

“The real killer has been the 1% TDS on each transaction,” said Ajeet Khurana, a crypto analyst and founder of Web3 platform Reflexical. “Because effectively this tax tells people not to transact. This has dampened sentiments the most.”

Foreign exchanges

While trading volumes crashed as much as 70% on Indian exchanges days after the imposition of the tax regime, the data shows website traffic for Binance remained more or less constant from June.

As for downloads, by July 22 – around three weeks after the start of the transaction tax – unique installations of Binance overtook all Indian exchanges.

“Effectively we have gifted volume to Binance,” Khurana said. “People will feel compelled to trade on international exchanges such as Binance because Binance will not implement the TDS.”

The move isn’t necessarily indicative of tax evasion, Khurana said. A notification from the income tax regulator said residents are supposed to calculate and file taxes themselves when an international exchange doesn’t implement TDS because it doesn’t fall under Indian jurisdiction.

In response to Parliamentary questions from opposition member of parliament Vivek K. Tankha on Tuesday, Pankaj Choudhary of the Finance Ministry said it does not register foreign crypto exchanges, and the same tax rules apply to anyone trading crypto irrespective of whether the exchange is registered in India or abroad.

The response also revealed that the government earned $7.3 million through TDS since its implementation.

"The amount of tax earned by the government shows that the actual net volume of all the exchanges combined is around 6,000 crores ($727 million) in Q3 2022 which is way below as compared to 2021, when the crypto market witnessed a massive bull run," said Shivam Thakral, CEO of Indian exchange BuyUcoin.

The “poorly designed 30% capital gains tax on crypto assets and sledgehammer approach of 1% TDS on exchange-traded transactions coincided with [the] global rout in cryptocurrencies to kill Indians' interest in cryptocurrencies,” said Subhash Garg, a former secretary in the Finance Ministry’s Department of Economic Affairs.

That’s evident not only in transactions but also in interactions with mobile platforms. Searches of keywords including “bitcoin” and “crypto” have dramatically declined, while negative terms such as “scam,” “waste” and “fraud” have increased on reviews and ratings of popular apps in the past 90 days, AppTweak’s data shows.

“Keyword search volumes (indexed between 5 as the lowest and 100 as the highest) reveal that the popularity of the keyword "bitcoin" fell from 72 to 34,” said Karan Lakhwani, AppTweak’s India head. “A similar trend was observed for the keyword ‘crypto,’ wherein keyword search volume fell from 81 to 37.”

Read More: Crypto Trading Volumes in India Collapse 10 Days After New Tax: Crebaco

Related news

Key U.S. Senate Republican Tim Scott Makes Crypto-Fan Debut

Stablecoin Default Guarantees Pose Risks to the Issuing Banks, Swiss Regulator Says

Crypto Use in Terror Financing Rises, but Is Still Relatively Small: Singapore

U.S. Presidential Candidate RFK Jr. Says He's 'Fully Committed' to Bitcoin

Jersey City to Invest in Bitcoin ETFs, the Latest Pension to Dive Into Crypto