What’s Next for Crypto?

After a staggering crypto rally, primarily led by Bitcoin, it is fair to say that the approval of spot bitcoin U.S. ETFs in January approval was a game-changer. Since January 10, crypto’s total market cap has surged from $1.5 trillion to $2.4 trillion, a 60% increase. Nonetheless, crypto remains a nascent and niche asset class – its size is only a fraction of gold (10%) and smaller than Microsoft ($3.1 trillion).

Many naysayers predicted that the ETF approval would be a classic buy-the-rumor-sell-the-fact situation. But, given the massive price rally, this could not have been further from the truth.

The burning question now is: What’s next?

You're reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

ETFs and Supply/Demand Imbalances

U.S. ETFs alone have attracted inflows of around $19 billion. Including all ETPs, the year-to-date figure is significantly higher. The Blackrock IBIT ETF is the fastest ETF to reach $10 billion in assets. In only two months, the ETF has amassed more bitcoin than Microstrategy since 2020.

These large inflows have created a supply/demand imbalance, thereby increasing the price of the underlying asset. Bitcoin ETFs in the U.S. alone account for ~4% of all Bitcoins in circulation. Add to this the fact that ~29% of all Bitcoin supply has not been touched for over five years, or might be lost forever, these ETFs now represent a significant source of demand.

The current demand-supply dynamics are likely to exacerbate once the Bitcoin halving takes place mid-April. Like a pre-announced corporate action in the traditional world, the event should not have any price impact. However, if the past is any guidance, halving cycles have acted as a psychological catalyst for price increases, kicking off a rally not only in Bitcoin but also in the altcoin market.

‘Crypto Is a Solution in Search of a Problem’

A large bulk of the flows into the ETFs has come from institutional investors, while retail investors have preferred buying coins directly. And this may be a key reason as to why this rally may still have legs. Unlike retail investors, institutional investors tend to have a longer-term investment horizon and are unlikely to sell all their ETF holdings as markets correct. While they do systematically rebalance from time to time, they are less susceptible to the day-to-day fluctuations compared to retail investors.

In that sense, the arrival of institutions may overall decrease the volatility of the asset class, making the asset class more embedded into the traditional financial system. This is still going to be a slow and gradual process, and while Bitcoin ETFs are certainly one catalyst, it is simply not enough for an entire asset class to become mainstream.

Although the crypto ecosystem is rich with applications ranging from use cases in payments, settlement, market-making, lending/borrowing, gaming, metaverse, logistics, art, copyright enforcement, and so on, it seems that most of these use cases are still either early-stage or focussed on a niche target group. For crypto to become mainstream, more real-world uses need to emerge and impact not just a tech savvy problem or user group, but offer tangible innovations to our everyday lives.

Where are we in the cycle and how to participate?

Looking at Google Trends, search results for terms such as “crypto” or “Bitcoin” have increased in recent weeks but remain a far cry from their peaks in the previous bull-market of 2021. Furthermore, the recent rally has been primarily led by Bitcoin and Ethereum. Altcoins have not had their big moment yet and most of them trade at a fraction of their all-time highs of November 2021. BTC dominance still hovers around 50%. Generally, altcoins tend to outperform Bitcoin and ETH in the later stages of the cycle. Given the favorable macroeconomic conditions, it seems like this rally could still have some room to go.

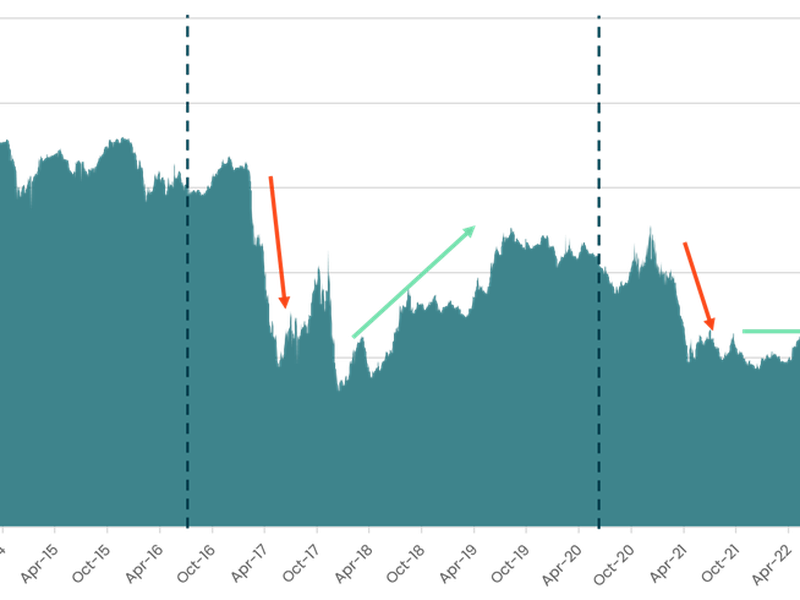

Figure 1 – Bitcoin Dominance and Halving

From a risk/return perspective, it appears as if cryptocurrencies may be compared to early-stage VC investing. Given that there are more than 9,000 cryptocurrencies in the world, it is probably safe to assume that a relatively small number of those will have a profound economic impact in our daily lives and thus would justify a long-term investment.

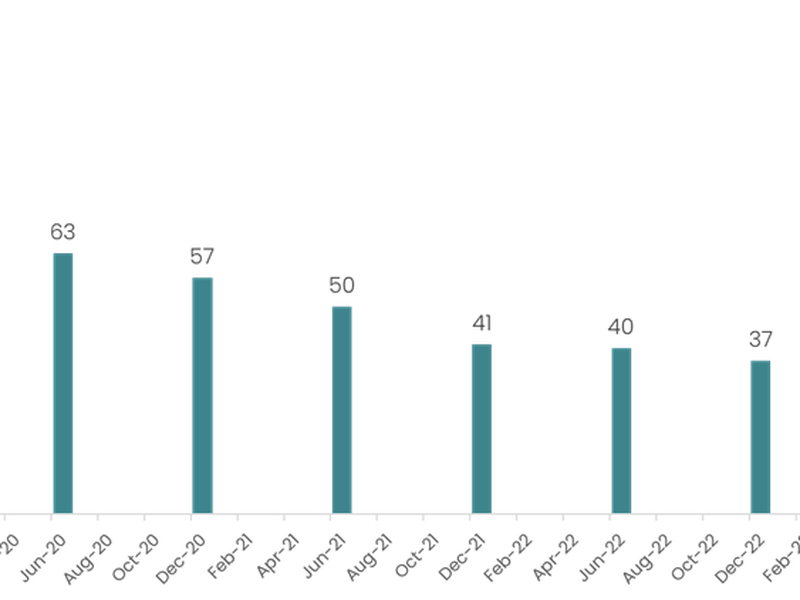

In Figure 1 below, we show how many of the top-100 tokens in June 2019 have maintained their place within the leaderboard over time. The numbers are sobering. In a similar way, the dotcom bubble showed how difficult it is to pick winners. Who would have thought that Amazon and Google would become the dominant companies within their industry back in the late-90s?

Figure 2 – How many of the Top 100 Coins in June 2019 Remain in Top 100 Over Time?

One way to avoid over-concentrated bets and refrain from chasing myopic trends, is to invest long-term in a broadly diversified buy-and-hold index. Having spent a considerable amount of time on index-engineering, we can see that a mix of quantitative and qualitative inclusion criteria, coupled with a smart-beta weighting methodology, provide the best results over an entire market cycle.

In the same way that there are not a lot of growth-equity stock pickers still around who outperformed the Nasdaq index since the late-90s, it is hard to imagine a world where individual coin pickers or discretionary market timers will outperform a rigorously designed index over the long run.

Related news

Bitcoin Chops Around $64K, With Japanese Yen's Tumble Maybe Signaling 'Currency Turmoil,' Analyst Says

NEAR and SHIB Led CoinDesk 20 Gainers Last Week: CoinDesk Indices Market Update

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M