What to Expect From Bitcoin in 2024

Optimism regarding a spot bitcoin ETF application approval ignited an almost 49% gain in BTC's price since October. It is likely that the Securities and Exchange Commission approves or denies multiple applications simultaneously for logistical and consistency reasons. (Figures cited are as of Dec. 18 unless noted otherwise.)

Spot BTC trading is concentrated on several exchanges: Coinbase, Binance, Bybit and OKX. They account for about 65% of spot BTC trading. Binance accounts for 35.5%, while Bybit, OKX and Coinbase account for 11.3%, 9.2%, and 8.9%, respectively.

The average BTC order size has been decreasing since early 2021 and is about $1,652. While smaller order sizes are associated with retail customers, many, if not most, institutions divide trade orders into smaller orders to minimize slippage. It would be imprudent to suggest retail customers were primarily responsible for recent trading patterns in BTC based on order size analysis alone.

You're reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

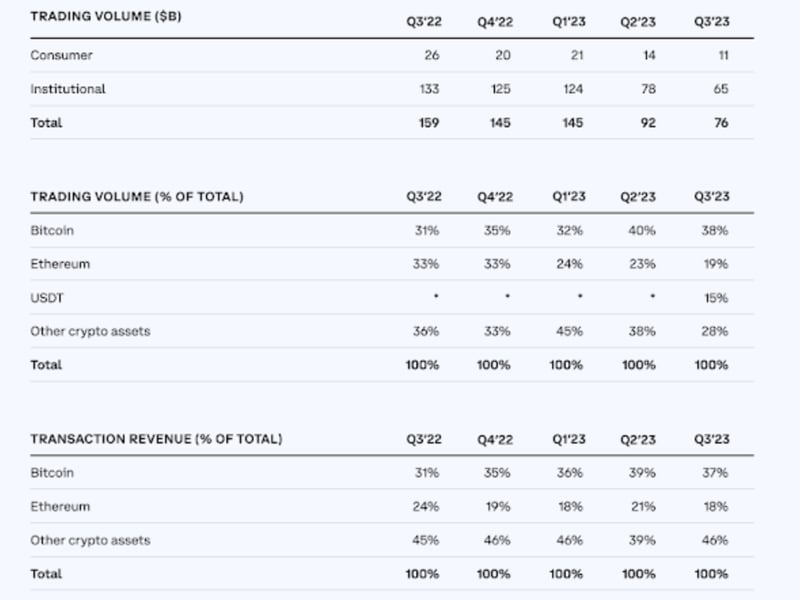

Coinbase's third-quarter 2023 trading summary suggests declining volume in three of the past four quarter-over-quarter measures. Volume among retail and institutional traders has fallen at a similar pace over the course of the past year, with retail and institutional customers trading about $4.2 billion and $24.7 billion in the third quarter, respectively.

Figure 1. Source: CoinBase, Path Digital Advisors

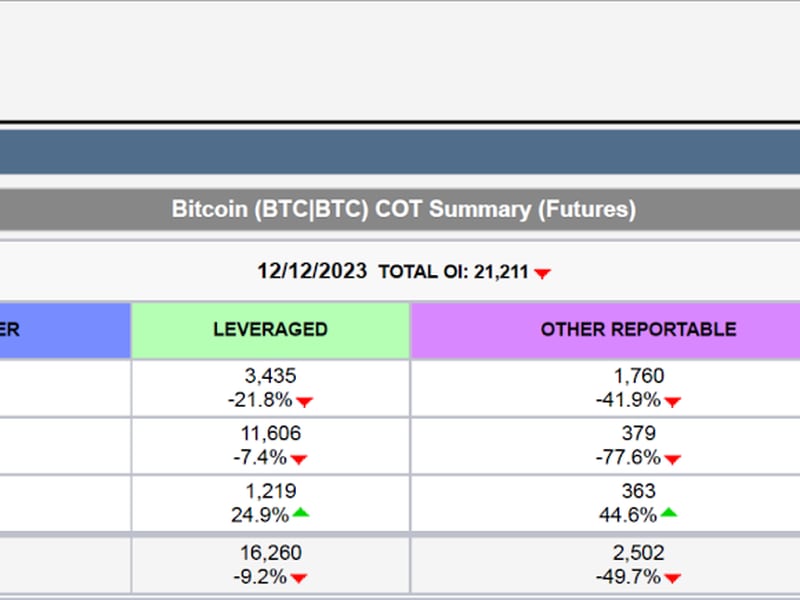

Bitcoin futures markets

CME Group's BTC futures open interest reached $4.55 billion, accounting for about 25% of total BTC open interest. Current open interest reached a level last seen in the second quarter of 2022.

Figure 2. Source: CME Group, Path Digital Advisors

The majority of CME BTC futures positions are held by asset managers and leveraged funds, with the former exhibiting a long bias and the latter showing a short bias. This appears intuitive as asset managers tend to approach investing with a longer time horizon relative to other buy-side customers. Conversely, hedge funds and commodity trading advisers, or CTAs, tend to trade with a shorter time horizon and engage in basis trading and hedging.

Institutional investors are becoming more active in the crypto space. CME Group notes that "average large Bitcoin open-interest holders, with at least 25 contracts, hit an all-time high the week of November 7, 2023."

The funding rate aligns the perpetual futures price to the spot price. When the funding rate is positive, long contract holders pay the funding fee to the short contract holders, and vice versa. The funding rate has trended higher with the spot price of BTC, suggesting bullish sentiment and bias.

Bitcoin outlook

The historical relationship between BTC prices and consumer interest has decoupled recently. If the antecedent that consumer interest is solely driven by retail customers is true, then it appears that either:

- Retail customers are trading without conducting research, or

- Institutional investors are having an outsized influence on prices.

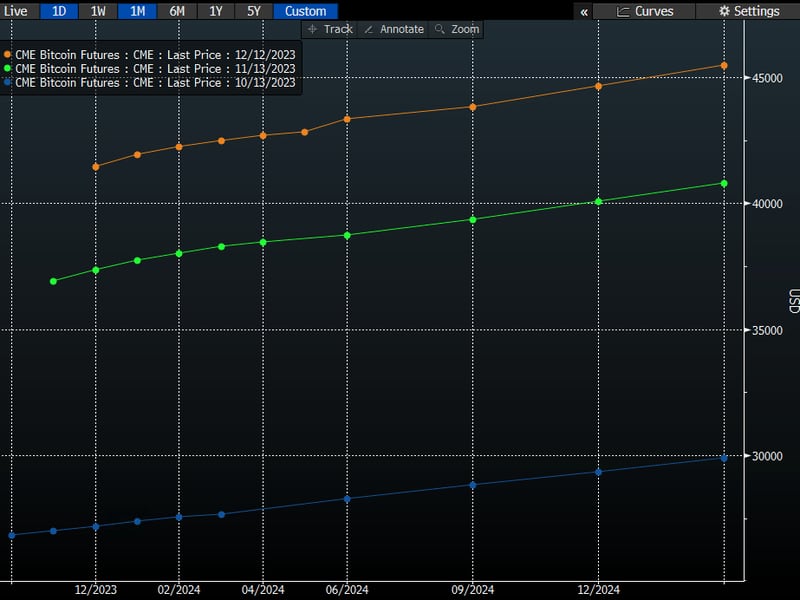

The sentiment among institutional investors appears to be constructive. The parallel upward shifts of the futures curve in each month of the fourth quarter of 2023 suggest bullish activity and a long bias among institutional investors.

The ETF approval is sufficiently baked into bitcoin prices such that positive momentum from the announcement may be offset by traders taking profits off the table. This suggests a possible reversion to the mean in the days after the announcement. Thereafter, the market will likely recalibrate its focus to the halving in April.

Figure 3. Source: Bloomberg, Path Digital Advisors LLC

Related news

Bitcoin Chops Around $64K, With Japanese Yen's Tumble Maybe Signaling 'Currency Turmoil,' Analyst Says

NEAR and SHIB Led CoinDesk 20 Gainers Last Week: CoinDesk Indices Market Update

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M