S&P Global Just Made Ethereum's Centralization Risk a TradFi Concern

In a recent note, S&P Global warned about the concentration risk present in Ethereum as Ether rallied in anticipation of a possible Ether exchange-traded fund (ETF).

"U.S. spot ether ETFs that incorporate staking could become large enough to change validator concentrations in the Ethereum network, for better or worse," S&P analysts wrote in a report published Tuesday. "It is therefore critical to understand how ETF issuers' choices will drive concentration risks."

S&P is right: concentration or centralization risk exists in all crypto. The fact that this is being discussed by traditional finance (TradFi) analysts once again (Morgan Stanley has flagged this before) shows just how much institutional interest there is in crypto post-ETF.

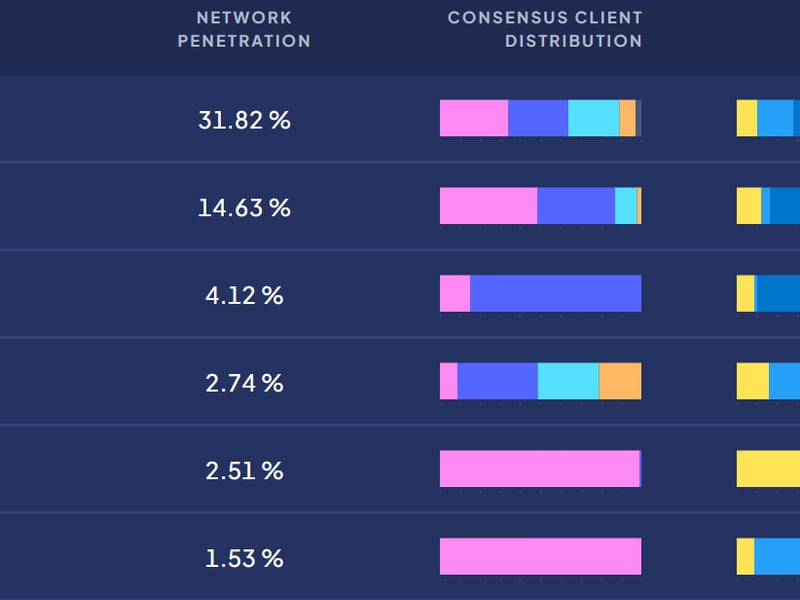

Lido, the largest Ethereum validator with just under 33% stake, and Coinbase, holding 15%, pose potential concentration risks, but a potential ether staking ETFs in the U.S., along-side spot ETFs, may reduce this by opting for institutional custodians and diversifying stakes across multiple entities, S&P analysts wrote in their report.

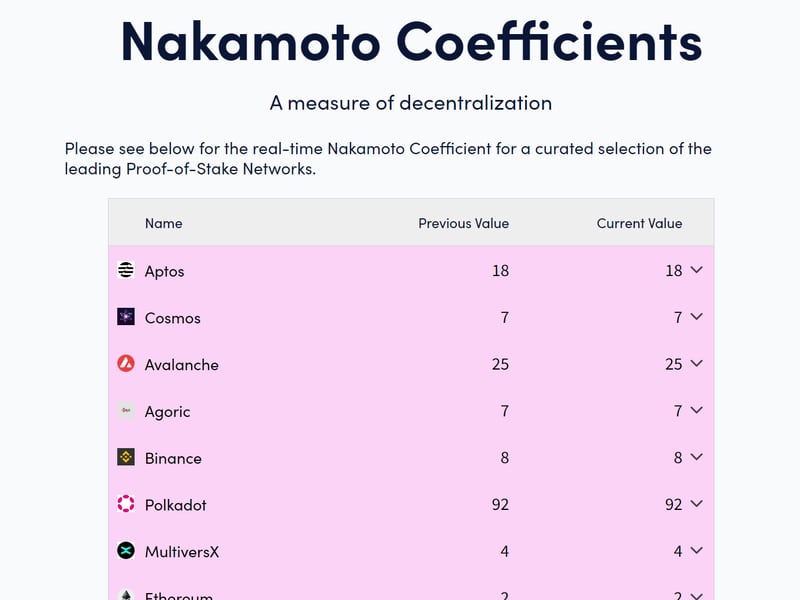

So, how centralized or concentrated is Ethereum? A good measure for this is the 'Nakamoto Coefficient,' which was first proposed by Balaji Srinivasan and Leland Lee. This measures a blockchain's decentralization by counting the nodes needed to control the chain. The higher the numbers, the better decentralization.

Right now, Ethereum's Nakamoto Coefficient is 2, which indicates serious concentration or centralization risk.

Networks like Aptos, Avalanche, or Polkadot have much higher numbers, indicating much more decentralization – but these protocols aren't being considered for an ETF because the SEC alleged that they are securities.

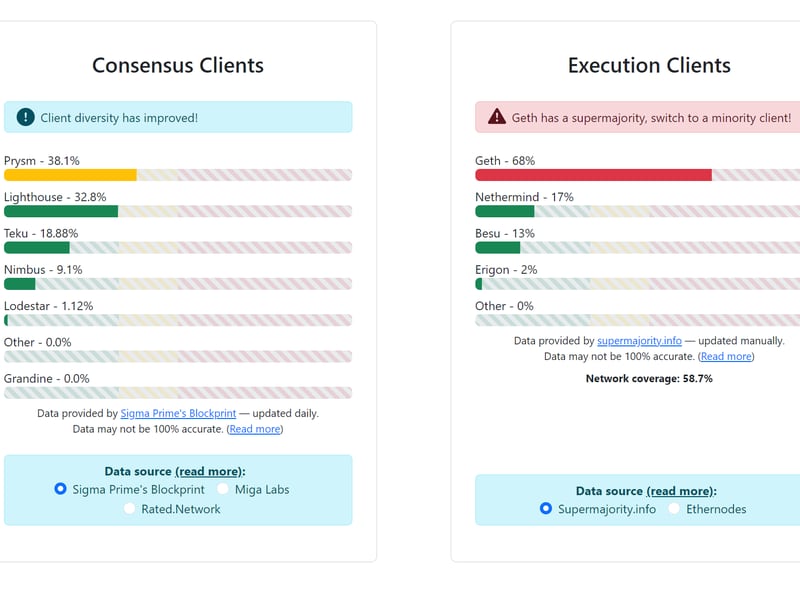

Parts of Ethereum's decentralization quandary have improved, but improvements elsewhere have been slow and stagnant.

For example, Geth - the most popular execution client for Ethereum - controls well over 60% of the execution client market, According to data from Clientdiversity.org.

Geth stands for "Go Ethereum," and is primarily developed and maintained by the Ethereum Foundation, the main nonprofit that supports Ethereum development. Geth is used to handle transactions, deployment and execution of smart contracts.

This is down from where it once was – when Geth controlled around 80% – but it is still a problem as it's still a supermajority.

Meanwhile, Prysm, a competing client, controls around 40% of the consensus client space.

As CoinDesk reported in January, a bug in Ethereum's Nethermind client software knocked out 8% of validators (it now controls 17%), raising concerns about what would occur if the same happened to Geth.

These numbers are improving. Perhaps the anticipation of institutional interest from a possible ETF will expedite the process.

Related news

Bitcoin Chops Around $64K, With Japanese Yen's Tumble Maybe Signaling 'Currency Turmoil,' Analyst Says

NEAR and SHIB Led CoinDesk 20 Gainers Last Week: CoinDesk Indices Market Update

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M