Experts Recommend Ether and Bitcoin Options 'Straddles' to Capture Post-Fed Price Swings

Investors who foresee renewed volatility in ether (ETH) and bitcoin (BTC) can consider building an option strategy that profits from an increase in price turbulence.

Markus Thielen, head of research and strategy at crypto services provider Matrixport, recommended buying short-term ether options "straddles" to benefit from potential price swings following Wednesday's all-important Federal Reserve rate decision.

Buying a straddle involves purchasing both bullish call and bearish put options with the same expiry and at the same level or strike price. Buying a call means purchasing insurance against bullish price moves while buying a put implies hedging against price slides. Option buyers pay a premium to sellers as compensation for offering protection.

When an entity buys a straddle, it's doing so in hopes that the underlying asset will either surge or tank enough to recover more than what was paid to purchase the strategy.

"Ether is expected to move by +/- 5.85% after the FOMC meeting, based on derivatives markets data. This implies that ether will finish the week at $1,485 or $1,670 (spot $1,578). This seems too narrow. Buying short-term straddles (buy calls and buy puts), which benefit from wide swings, might offer good risk reward here," Thielen said in a note sent to clients early Wednesday.

Expectations for post-Fed price turbulence appear underpriced and options tied to Ethereum's native token look cheap. The annualized one-month ether implied volatility, or traders' expectations for price turbulence over four weeks, currently stands at 81% versus 96%, seen ahead of the September Fed meeting, according to data tracked by Matrixport.

Implied volatility has a positive impact on options prices. Traders often compare implied volatility over specific periods to gauge whether volatility expectations are overpriced/underpriced and options are trading cheap or costly. The common mantra is to buy options when implied volatility is cheap relative to its historical standard/realized volatility and sell options when the implied volatility is too high.

"Implied volatility is roughly 15 vol points lower compared to the last FOMC meeting, which makes option prices significantly cheaper than at the last FOMC meeting," Thielen noted.

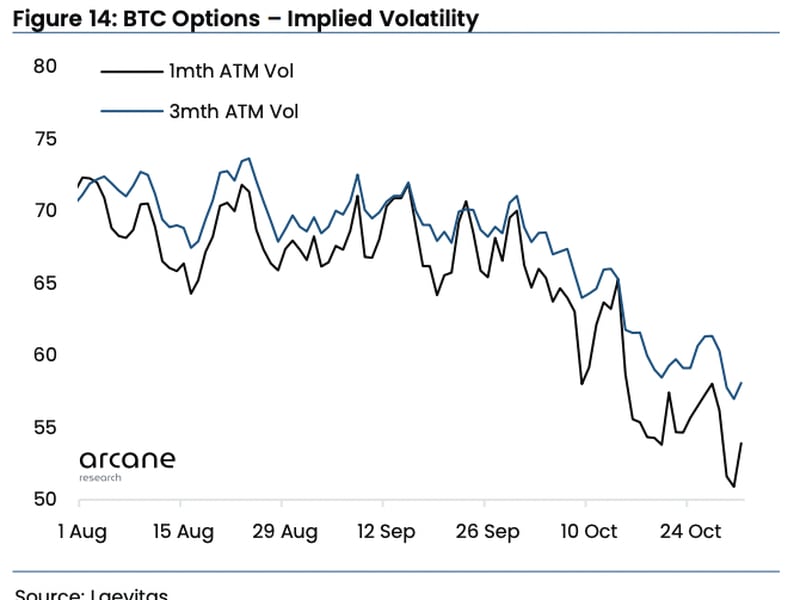

The bitcoin market has seen a similar "implied volatility meltdown" in recent weeks, making options cheaper.

Bitcoin's annualized three-month implied volatility recently slipped to nearly 50%, a level seen only five times since 2020. The one-month implied volatility dropped to 56%, according to data from Arcane Research and derivatives analytics platform Laevitas.

"The low implied volatilities are a suitable environment for contrarian bets on reappearing BTC volatility," Lunde wrote in a note to clients on Tuesday.

"The timing could be great for straddle strategies purchasing far-dated expiring puts and calls. Straddles look cheap." Lunde added.

Straddles look simple, but they are not without risks. A trader can lose the entire amount paid as compensation to call and put seller if the market stays flat.

That said, several key events are lined up for the coming weeks, promising to inject volatility into markets.

"Traders should prepare for volatility in the coming weeks, as the event calendar is crowded with potentially market-moving events. Wednesday's FOMC press conference is this week's key event, but company earnings (MicroStrategy Nov 1, Coinbase Nov 3), economic data, and U.S. mid-terms may also lead markets to move," Lunde said.

Bitcoin traded near $20,400 at press time. The cryptocurrency has been dead flat for nearly two months, barring the past week's minor spike of 5%, CoinDesk data show.

Ether changed hands at $1,570, according to CoinDesk data.

Related news

Bitcoin Chops Around $64K, With Japanese Yen's Tumble Maybe Signaling 'Currency Turmoil,' Analyst Says

NEAR and SHIB Led CoinDesk 20 Gainers Last Week: CoinDesk Indices Market Update

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M