Ether Futures See Unusually High Liquidations as Funding Rates Point to Bearish Sentiment

Futures tracking ether (ETH) have racked up almost $140 million in liquidations over the past 24 hours with a key metric suggesting traders are turning bearish on the asset's near-term growth as they focus their attention on the contracts before Ethereum's Merge next month.

Liquidations occur when an exchange forces a trader’s leveraged position to close because of a partial or total loss of margin, or funds set aside to keep the trade open.

According to Coinglass data, liquidations on bitcoin futures hovered at $54 million over the same period, with other major cryptocurrencies, such as solana and avalanche, seeing just over $3 million. Bitcoin futures usually have the highest liquidations in the futures markets owing to their popularity and liquidity.

Ether's recent popularity suggests there's currently higher interest for that market in the absence of a notable catalyst for bitcoin. In the past month, weekly trading volumes on spot ether have surpassed those of spot bitcoin for the first time, data from research firm Kaiko show.

Volatility in ether since Aug. 29 sent the price to over $1,600 on Tuesday morning from $1,420 followed by a decline to $1,472 on Tuesday evening and back above $1,620 on Wednesday morning.

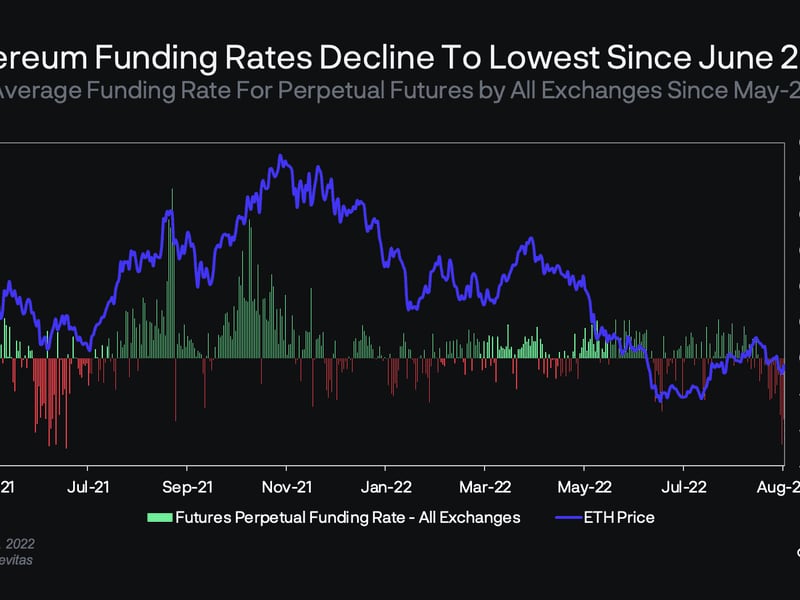

Some analysts have pointed to funding rates in futures markets as a source for the price volatility. They also say the rates could lead to a short squeeze. A short squeeze refers to a sharp price increase that forces traders who had sold a borrowed asset in anticipation of repurchasing it at a lower price – a strategy known as shorting – to close out their positions, usually leading to a further increase in prices. Shorting an asset means betting its price will fall.

Funding rates are periodic payments made by traders based on the difference between prices in the futures and spot markets. Depending on their open positions, traders will either pay or receive funding. The payments ensure there are always participants on both sides of the trade. Participants utilize sophisticated strategies to collect funding rates while hedging losses due to token movements.

Funding rates for ether futures slid to a yearly low of -0.024% on Aug. 27, analysts at Delphi Digital said in a report this week. Similar levels were last seen in June 2021 and followed by a massive short squeeze the following month, the analysts said.

Open interest on ether contracts has remained above $5 billion, the analysts said. Most is “likely to be short as funding rates have flipped negative from August 14,” they said.

When rates are positive, long traders – who own the asset – pay short traders. This implies that traders are generally bullish as they are willing to pay the funding rate to keep their long positions open. Negative rates imply traders are generally bearish.

Negative funding rates, however, may also indicate that traders are hedging their spot ether holdings by shorting the asset using futures. This allows traders to protect losses in case ether prices fall while receiving the proposed ether proof-of-work tokens (ETHPOW) at the time of the Merge. But rates have turned and remained negative for over two weeks, suggesting higher demand from traders to remain short on ether contracts.

Some traders say broader equity markets have more of an impact on ether prices than technical catalysts like the Merge.

“Looking at the charts of both ether and Nasdaq 100, one gets the impression that there may be a strong correlation between the two contracts since the beginning of the year,” Daniel Kostecki, director at financial services firm Conotoxia, told CoinDesk in a Telegram message. He noted that poor sentiment in traditional equity markets may be driving prices of ether more than “the anticipation of the Merge.”

“It seems that it may now be difficult for both ether and other cryptocurrencies to break this correlation,” Kostecki said.

Related news

Bitcoin to Account for 7% of Global Wealth, Surge in Price to $13M in 21 Years: Michael Saylor

CoinDesk 20 Performance Update: RNDR's 12% Gain Leads as Index Rebounds

First Mover Americas: Bitcoin Regains $67,000, Adds Nearly 5% in 24 Hours

Elon Musk’s X Quietly Removes Bitcoin, MAGA Emojis From Hashtags

Bitcoin Analysts Express Optimism as Price Nears Resistance Level That Stymied It in May