Crypto Market’s Near-Apocalypse in 2022 Turns Zombie Tokens Into Dead Coins

When the decentralized marketplace Storeum debuted its own freshly minted cryptocurrency in July 2019, the STO token soon grabbed traders’ attention: The STO price jumped from a few cents to an all-time high around $35 for a few days in March 2020 before quickly settling back to less than $1.

But Storeum has since gone mostly quiet. Its website no longer works and social media accounts are inactive. The token technically still exists, in zombie form, as a contract on the Ethereum blockchain. This year, the STO has taken another step toward oblivion: It has vanished from the pricing site CoinGecko, which lists nearly 13,000 cryptocurrencies that are still considered viable in some form.

CoinGecko officials would not confirm when exactly Storeum was deactivated from its website. But a cursory search using the Wayback Machine, which archives websites from prior dates, shows that a Storeum token page was still active as of early 2022. Now, typing Storeum into CoinGecko’s search bar turns up no results.

Call it a dead coin.

During the crypto bull market of recent years, the number of cryptocurrencies seemed to be ever-increasing, roughly quadrupling from 2019 through early 2022, based on data from the website Statista. Since peaking at 10,397 in February 2022, the number has dropped by about 1,000, the biggest-ever decline in the 13-year-old crypto industry’s volatile history.

“It’s relatively simple for someone to create a token,” said Riyad Carey, research analyst at crypto data firm Kaiko. “But these tokens can obviously lose interest extremely quickly.”

Just as STO arrived during an earlier crypto bull-market hype cycle, a bevy of tokens appeared last year as bitcoin (BTC) – the oldest and largest cryptocurrency, often viewed as an industry bellwether – shot to a record $69,000.

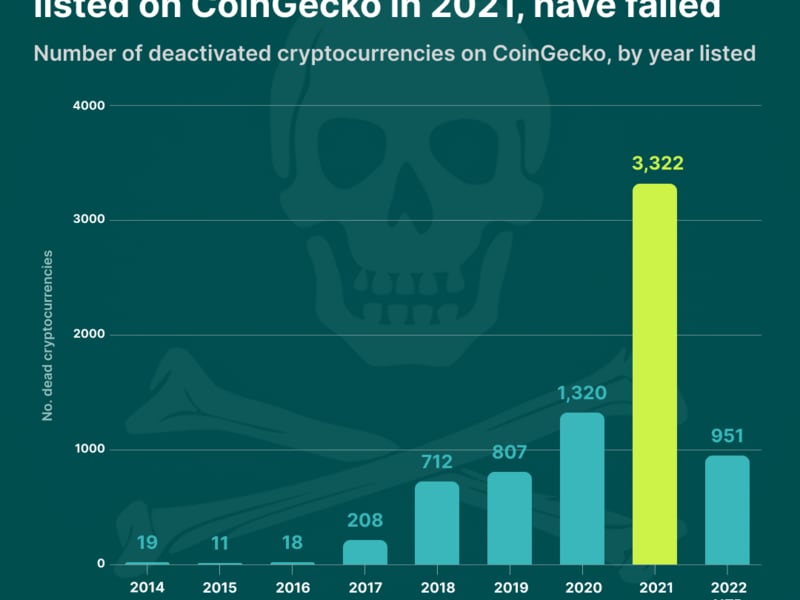

According to CoinGecko, which uses a different methodology from Statista’s, over 8,000 cryptocurrencies were newly listed in 2021, but some 3,300 of them, or roughly 41%, ended up being deactivated and delisted.

“During this period, many cryptocurrency projects, tokens and coins with little to no value or any immediate or discernible purpose were launched by various anonymous developers,” Julia Ng, growth marketing at CoinGecko, wrote in a recent analysis. “Few were actually committed to their projects, which resulted in a high rate of failure, and thus their ultimate demise.”

Tokens might be removed from the site due to a lack of any discernible trading activity within the last two months, based on CoinGecko's methodology. A coin might also be taken off CoinGecko if it's deemed to be a "rug pull" or other scams, or if the project team requests a deactivation.

"This might occur when the team disbands, rebrands, shutters the project, or undergo major token overhauls where old tokens become sufficiently illiquid or dead, according to CoinGecko standards," Ng wrote.

The overall crypto market’s capitalization has shrunk from an all-time high of $3 trillion in November 2021 to about $850 billion now. Bitcoin’s price has fallen 66% over the past year and ether (ETH) is down 71%.

Kaiko’s Carey estimated that the number of failed tokens could be “significantly higher in the past two years” because of the explosion in 2017 in the number of ERC-20 tokens – a type that’s easy to mint and runs atop the Ethereum blockchain.

“It’s relatively simple for someone to create a token and an associated decentralized exchanges [DEX] liquidity pool,” Carey told CoinDesk. “If no one is providing liquidity, there will be little or no trading volume.”.

Rug pull

Besides losing buyers’ interests, some token failures could be associated with scams, according to Chainalysis Director of Research Kim Grauer.

One of the more common schemes, referred to in the gallows-humor jargon of crypto traders as the “rug pull,” involves “creating a token, funding the liquidity pool, and then removing all the liquidity after an initial rush of people buy the token,” as Carey describes it.

As is the case with Storeum, the contract behind the token remains on the blockchain; the data is still there, for posterity, even when the token has gone dormant and is long forgotten. Etherscan, a data explorer for the Ethereum blockchain, shows no transactions have occurred for 231 days.

A warning notice on the Etherscan page reads, "Warning! There are reports that this token used a fake team profile on their website. Please exercise caution when interacting with this token."

At one point, back in 2019, there was chatter on the forum bitcointalk.org that the Storeum project might be a "scam hitting on all cylinders," including speculation that team members were ginned up using artificial intelligence.

Chainalysis’s Grauer told CoinDesk that “it is difficult for a token to totally ‘die’ because the code keeps the project running even without buyers.”

The existence of dead coins points up a key paradox of the crypto industry, according to Kaiko's Carey: Decentralization, often portrayed as a pillar of virtue, can proves to be little more than an illusion. Just like the fast growth.

It's “decentralization, in that the bar to creating tokens has been dramatically lowered in recent years,” Carey said. It's “centralization, in that many of these tokens or projects relied on one or a few individuals to provide liquidity and keep the project alive. Centralized exchanges are well within their right to remove tokens with little or no trading volume, as they won’t contribute to revenue and likely entail some cost to upkeep.”

Some tokens might be better off dead.

Related news

Kara Swisher Downplays Crypto's Significance: 'It's Not the Center of Everything'

Bitcoin Dips to $63K as Rate Cut Hopes Dim Following Disappointing U.S. Inflation Report

First Mover Americas: Bitcoin Drops Below $64K, Ether Falls

BlackRock's Bitcoin ETF Snaps 71-Day Inflows Streak, Data Show

Why Base Chain Has Potential to Lock the Next Generation of Crypto Users