Bitcoin Options Market Still Afraid of USDC Volatility

The Circle-issued USDC stablecoin regained its dollar peg, recovering from the Silicon Valley Bank-induced chaos over the weekend that saw its price plummet to $0.90 on major exchanges.

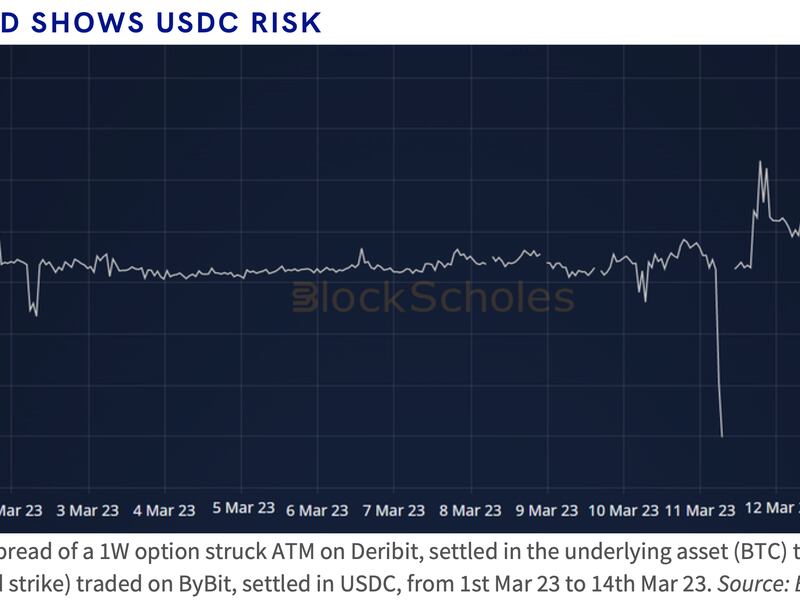

The re-pegging is yet to calm nerves in bitcoin's derivatives market, where Deribit-listed options contracts settled in BTC trade at a higher implied volatility (IV) premium than Bybit's contracts paid in USDC.

That's a sign of investor preference for contracts settled in native cryptocurrencies, according to crypto derivatives analytics firm Block Scholes.

"Whilst USDC has now recovered its peg to trade at $0.99, the [positive] spread of Deribit option- to ByBit option-implied volatility persists," Andrew Melville, research analyst at crypto derivatives analytics firm Block Scholes, wrote in Tuesday's research note.

"The discrepancy is present across the term structure and is most dramatic at longer tenors [longer duration options]. This suggests that the market is still valuing options that settle in the underlying (rather than USDC) at a relative premium due to a continued concern of a further depeg," Melville added.

Options are derivative contracts that give the purchaser the right but not the obligation to purchase the underlying asset at a predetermined price on or before a specific date. A call option gives the right to buy, while the put option offers the right to sell.

Implied volatility (IV) refers to the options market's expectations for price turbulence over a specific period. Higher implied volatility represents increased demand and prices for options. Volatility term structure is the graphical representation of how options of the same underlying asset exhibit different implied volatilities across different expiration months.

Bybit and Deribit calculate the payoff or profit/loss from the options trade, referencing the dollar value of the underlying asset (BTC). However, at Deribit, the actual settlement is paid in BTC, while Bybit uses USDC. Settlement refers to resolving the contract between trading parties through exchange of cash or actual underlying asset.

That exposes Bybit-based options traders to volatility in USDC. Besides, a potential crash in the stablecoin would make Bybit's options worthless.

"The brief depeg of USDC tokens to $0.90 meant that options on Bybit would be settled at around 90% of their stated payoff in dollar terms. The market was slow to price for this difference, briefly continuing to price both option-types at the same level of implied volatility," Melville said.

The spread between the seven-day IV derived from Deribit and Bybit-listed options surged over the weekend and has remained elevated ever since.

"Although the decoupling crisis between USDC and USD has been temporarily lifted, investors are unwilling to take systemic risks, so [options] buyers will seek lower premiums in the far-end options," Griffin Ardern, volatility trader from crypto asset management firm Blofin, told CoinDesk.

Related news

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M

Kara Swisher Downplays Crypto's Significance: 'It's Not the Center of Everything'

Bitcoin Dips to $63K as Rate Cut Hopes Dim Following Disappointing U.S. Inflation Report