Are Rising Yields Putting the Squeeze on DeFi?

In the ever-evolving world of digital assets, Ethereum is facing the squeeze of diminishing demand amid rising U.S. Treasury yields. This is evident in the ether (ETH) staking rate, which is the reward paid to validators to support the operation of the Ethereum network. According to the Composite Ether Staking Rate (CESR) index, this rate continues to hover around 3.7% annualized, less than half the rate back in June of 8%, as rewards from fewer network transaction fees are spread across a larger number of validators.

Unfortunately, this reward from staking ether falls short of the 5% yields provided by U.S. government bonds – basically the safest assets in the world and the benchmark investment from which all other investments are evaluated within the existing financial system.

You’re reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

So, are we done here? Does this shake the very foundation of the Ethereum network and eliminate the potential buoy that was keeping ether prices afloat? Through all the ups and downs of the broader CoinDesk Market Index, were ether token holders simply chasing yield? Before you reach for your cold storage wallet and fire up MetaMask, let’s dig in a bit to fill in details around this overly simplistic prevailing narrative.

It's important to acknowledge that comparing U.S. fixed income yields to ether staking yields is not exactly an apples-to-apples comparison. This is because it fundamentally juxtaposes:

- a fixed nominal yield exemplified by Treasuries against an inflation-adjusted real yield

- a low-risk capped price (i.e. par value) asset with a volatile growth asset

Furthermore, since last year's Ethereum Merge, there has been no significant net issuance of new ether tokens, while the U.S. Treasury has increased issuance by 25% year-over-year (as of September) to finance ever increasing budget deficits.

Putting aside this fixed nominal versus real yield growth asset income comparison, the wait times for Ethereum validators (another proxy for Ethereum demand) has reduced significantly, from 44 days in June to merely a day, according to Validator Queue. While this may indicate that the demand imbalance in the market has rectified, it may also signal a lack of overall interest in Ethereum post-Merge.

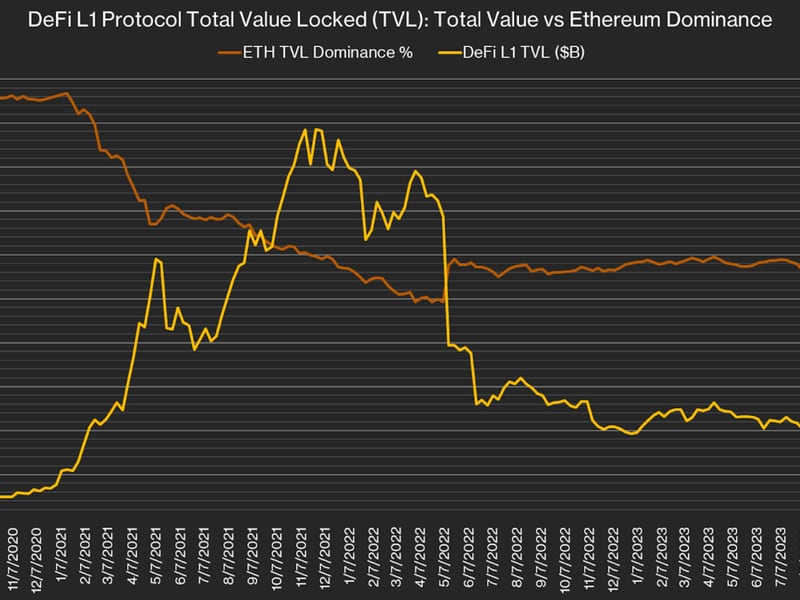

To gauge this ether demand more comprehensively, it's valuable to look across the entire decentralized finance, or DeFi, space, to examine the relative total value locked (TVL) within the Ethereum level-1 protocol and compare it to the total value locked across other competing L1 blockchains within the CoinDesk Smart Contract Platform Index. Despite the introduction of newer L1 chains and protocols, Ethereum has retained the lion's share of TVL, holding steady at 54% and fluctuating between 50% and 60% of TVL over the past two years. This is especially noteworthy considering this period includes the crypto winter.

(Source: DefiLlama)

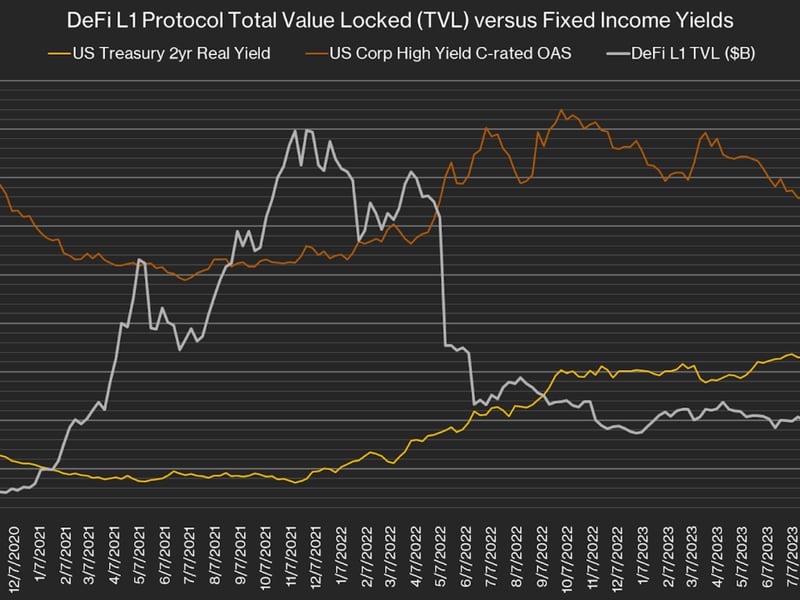

One takeaway from the TVL data is the ongoing exodus of capital from L1 chains. TVL has shrunk from its peak of $180 billion during the height in late 2021 when the Federal Reserve began raising interest rates in response to escalating inflation. When viewed across Treasury and corporate credit market rates, it's apparent that the decline in TVL has coincided with the surge in borrowing costs and tightness in lending and credit standards, as demonstrated by the C-rated corporate bond option adjusted spread (OAS) over Treasuries.

(Source: DefiLlama, St. Louis Fed)

The correlation between weekly changes in DeFi TVL and changes in traditional finance, or TradFi, market yields is also statistically significant, with every 100-basis-point increase in real yields and the high yield C-rated OAS leading to an anticipated 14% and 4% reduction in DeFi TVL, respectively. After correcting for these TradFi yield effects, DeFi TVL still managed to grow at an average rate of 1.6% per week over this period. This relationship dynamic demonstrates that, while capital locked on-chain can be employed for various activities (i.e. yield farming, staking and trading), returns on capital are fundamentally benchmarked (and possibly financed) against the opportunity to hold relatively risk-free, short-term fixed income securities, barring the long-term risks of inflation and debasement.

While this may not bode well for the short-term prospects of L1 protocols' TVL and on-chain transaction activity, understanding the linkage between traditional markets and DeFi markets is essential for developing an actionable investment strategy for when real and nominal interest rates inevitably decline to stimulate the economy in the backdrop of an economic slowdown.

However, we may not see a zero interest rate environment come back anytime soon, as the recent sell-off in longer-dated bonds reflects a growing acknowledgment that the equilibrium rate of interest (formally known as "R-star" – no association with Ringo) may settle at higher levels than previous rate cycles, even after inflation aligns with the Fed's 2% target.

This higher neutral rate of interest is the equilibrium rate of interest that does not produce changes in inflation, and is shaped by factors such as technology, demographics and overall economic productivity, and may persist higher for longer than we’ve witnessed over the past decade in markets.

If digital assets and DeFi applications can produce significant value and utility to the real economy (i.e. tokenizing real-world assets), then blockchain staking rates and DeFi activities will have no problem competing for future capital against other investment opportunities within the broader traditional financial system. However, without these real-world applications and given the current trajectory of rising real yields, a giant sucking sound continues to persist in the world of DeFi.

Takeaways

From CoinDesk Deputy Editor-in-Chief Nick Baker, here is some news worth reading:

- BITCOIN $35K: Flash crashes have gotten a fair amount of attention over the years. These sudden – very sudden – price drops tend to get old-school traders worked up about how computers are ruining markets. Anyway, flash rallies don't get the same attention, but, even if it wasn't really a computer-driven flash rally, what just happened with bitcoin (BTC) sure felt like one. On Monday, BTC surpassed $31,000 for the first time in months. And then, in just a few minutes, it briefly leapt above $35,000. Optimism about bitcoin ETF prospects and also options-market mechanics were some of the explanations. Whatever the cause, bitcoin has doubled in price this year and crypto is starting to feel surprisingly ebullient.

- A BORING WEBSITE: Why did people get so excited about bitcoin ETFs and their odds of winning U.S. approval? A normally boring website for the normally boring Depository Trust & Clearing Corp. I've told more than one young financial journalist over the years that clearing is a vital part of financial markets, yet it's generally a dull topic, so it's important when writing about clearing to stress the former to overcome the latter. But it turns out DTCC can spark excitement! BlackRock's proposed ETF showed up on a DTCC webpage, complete with a CUSIP and ticker symbol. Crypto folks thought that was good news, maybe even a sign BlackRock's application had been approved. It definitely didn't mean that, though it's not exactly bad news that BlackRock is completing this prep work, getting a CUSIP and ticker, etc. This possibly misguided optimism likely fueled some, or maybe even most, of Monday's big bitcoin rally. But boring websites giveth and boring websites taketh away. By Tuesday, BlackRock's ETF had vanished from the DTCC site. Bitcoin fell. Later in the day, DTCC revealed something to CoinDesk that meant people probably shouldn’t have gotten so worked up this week: The BlackRock ETF has been on that page since August.

Related news

Bitcoin Chops Around $64K, With Japanese Yen's Tumble Maybe Signaling 'Currency Turmoil,' Analyst Says

NEAR and SHIB Led CoinDesk 20 Gainers Last Week: CoinDesk Indices Market Update

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M