A Year After Debut, ProShares Bitcoin ETF Has Underperformed Market By 1.8%

ProShares' bitcoin (BTC) futures exchange-traded fund (ETF) went live on the New York Stock Exchange (NYSE) a year ago, allowing investors to take a bullish exposure to the world's largest cryptocurrency without having to own it.

Since its debut, the long BTC futures-based ETF has underperformed bitcoin by 1.79%, according to data tracked by Arcane Research. In other words, the ETF, trading under the ticker BITO on NYSE, has bled slightly more than bitcoin, which has declined nearly 70% since the fund's launch date of Oct 18, 2021, according to CoinDesk data.

However, the ETF has fared well compared to market expectations. After inception, several observers were worried that BITO would underperform bitcoin by 10% to 13% due to contango bleed – the cost associated with rolling or moving the long (buy) position from an expiring contract to the next month's contract.

"While bad, the underperformance was far lower than estimated based on 2021 data, forecasting 13% annualized rolling costs," Arcane Research's Vetle Lunde said in a note sent to clients early this week.

Explaining the contango bleed

Before diving into what helped BITO outperform market expectations, it's imperative to understand the inner workings of the fund that make it vulnerable to contango bleed.

BITO purchases bitcoin futures listed on the Chicago Mercantile Exchange (CME) rather than the actual cryptocurrency.

The futures market typically trades in contango – a situation where the futures price exceeds the spot price. However, as expiry nears, the contract due for settlement erases the premium and converges with the spot price, while the next month's contract continues to trade at a premium.

Therefore, when the fund rolls over long positions, it liquidates expiring contracts at a price lower than the cost at which it was acquired and then purchases the following month's contract at a premium to the spot price. Essentially, the fund sells low and buys high on every expiry, bleeding money and ultimately underperforming the underlying asset.

Perhaps holding the actual cryptocurrency is the best bet irrespective of market trends.

Bear market saved the day

The crypto bear market, which began late last year, reduced monthly rollover costs and likely helped the fund beat market expectations, according to Arcane's Lunde.

The degree of the contango bleed depends on how steep the contango is. It's usually steeper during a bull market when an asset is expected to rise and flattens during bearish trends.

As bitcoin began falling in December last year, the spread between prices in futures and spot markets collapsed. The annualized premium in three-month CME-listed futures slipped into single digits from nearly 20% in April 2021.

The premium fell as low as 3% in January this year and has remained mostly below 5% ever since, barring occasional backwardation – a situation where spot prices are greater than futures prices.

As such, monthly rollovers became cheaper, ensuring BITO bleeds less money than previously anticipated.

"Due to a structural market shift as BTC brutally entered a prolonged bear market after the massive liquidation event on Dec. 4, 2021, CME’s futures have tended to trade in a flat structure with minimal contango and periodically in backwardation," Lunde noted.

"Rolling dynamics have played in investors' favor in 2022," Lunde added.

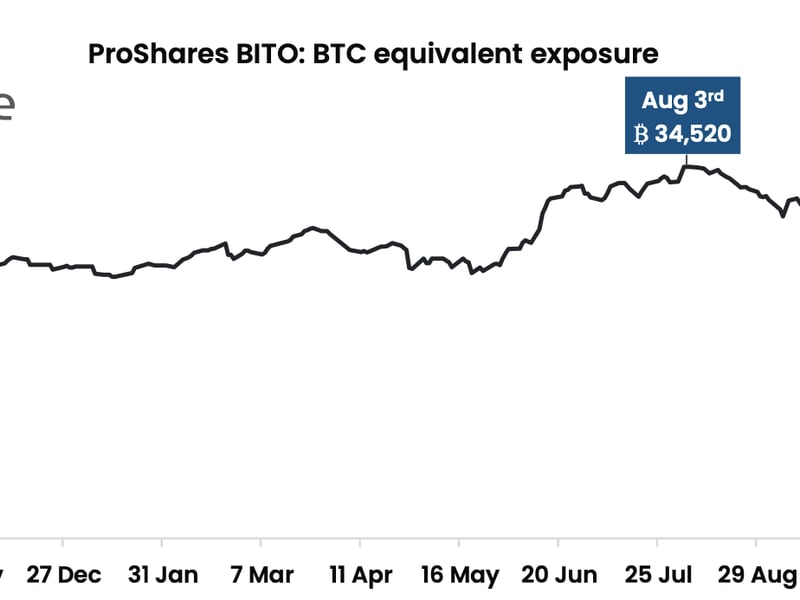

Record exposure

While the contango bleed makes futures-based ETFs look inferior to spot-based ETFs, investors seem to appreciate what they got. (U.S. regulators continue to reject spot-based ETFs).

Early this week, ProShares held a long exposure on CME equivalent to 32,520 BTC ($620 million), matching the August peak. VanEck and Valkyrie's funds, which went live after ProShares' debut, held a bullish exposure of 1075 and 1095 BTC, respectively.

According to Arcane Research, futures-based ETFs from ProShares, VanEck, and Valkyrie account for half the open interest on the CME. Open interest refers to the dollar amount locked in the number of contracts open at a given time.

Related news

Bitcoin Chops Around $64K, With Japanese Yen's Tumble Maybe Signaling 'Currency Turmoil,' Analyst Says

NEAR and SHIB Led CoinDesk 20 Gainers Last Week: CoinDesk Indices Market Update

First Mover Americas: Bitcoin Holds Stable as ETF Outflows Increase

ARK Sells Last of Its ProShares Bitcoin Futures ETF Shares

Bitcoin Stable Above $64K While ETF Outflows Hit $200M