A Dose of 'Hopium' for Bitcoin Bulls From 1970s

The question of whether inflation has peaked is passe for risk assets, including cryptocurrencies.

There has been a slowdown in the inflation rate in the U.S. and other parts of the world since the third quarter of 2022. In response, the Federal Reserve (Fed), the world's most powerful central bank, has slowed liquidity tightening that pushed cryptocurrencies and stocks into a bear market last year.

The question now is whether the turnaround is enough to lift risk assets.

The answer is yes, according to data that show the S&P 500, Wall Street's equity index and a benchmark for risk assets worldwide, tends to bottom out and rally when the consumer price index (CPI) peaks. Bitcoin has historically moved more or less in line with U.S. stocks.

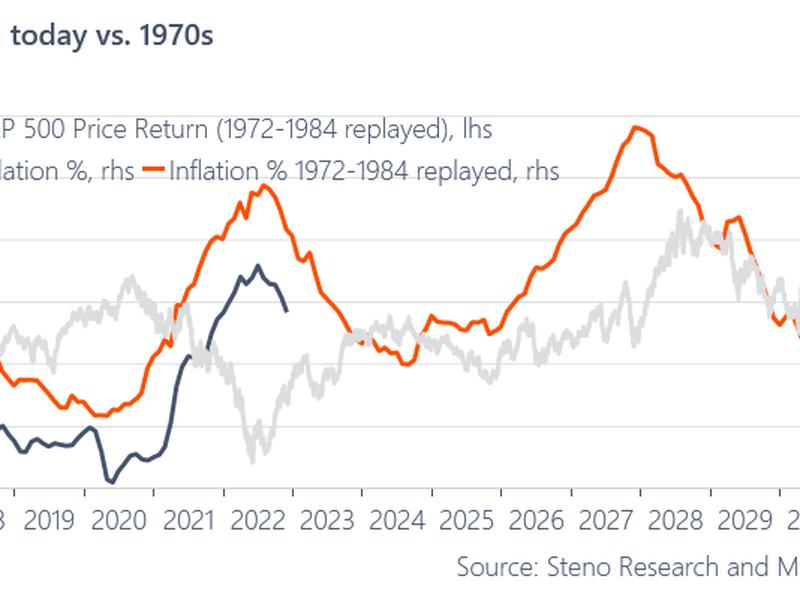

The chart by Steno Research and Macrobond compares the U.S. CPI trajectory from 2018 to date with its 1972-1984 path and adds the S&P 500's performance during the 1970s.

The index bottomed out around the end of 1974 as the CPI peaked, then rallied over 50% in the next 21 months. A similar pattern occurred after CPI logged its second peak in March 1980.

The U.S. CPI's trend from 2018 to date looks analogous to the pop and drop of the early 1970s, meaning further deceleration in inflation and a revival in risk assets could be on the cards.

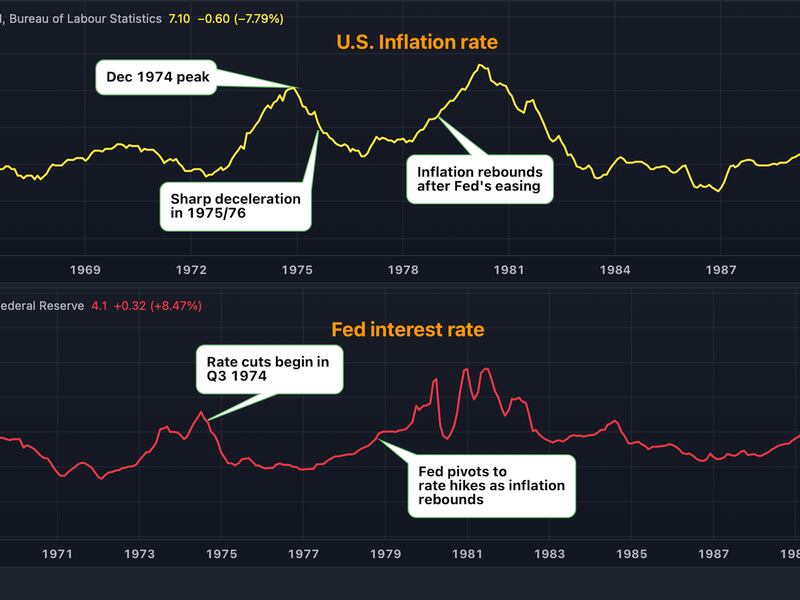

"The 1972-1984 playbook shows how equities bounced right as the CPI peaked even as the earnings outlook deteriorated markedly at the same time," Andreas Steno Larsen, founder and CEO of Steno Research, said in a note published on Dec. 26, explaining reasons to begin 2023 with a bit of risk exposure. "If the market sniffs out an inflation-driven pause or a pivot from the Fed, even before a drawdown in risk assets is seen, we may get a disinflation rally that will wrong-foot all investment banks."

Many investment banks and financial commentators on Twitter have penciled in a continued slide in risk assets in the first half of this year that will force the Fed to abandon policy tightening.

The rate of U.S. consumer inflation cooled to 7.7% in November 2022 from a four-decade high of 9.1% in June. The Fed stepped down to a 50 basis-point rate increase in December after delivering four consecutive 75 basis-point hikes. The bank, however, signaled a higher rate peak in the range of 5% to 5.25%.

Limited upside

Still, some observers remain cautious.

"An analog to the stagflationary 1970s shows that while the inflation downturn is imminent, it is likely it will not reach the Fed's 2% target. More worryingly, there is also a risk of a V-shaped rebound if the Fed loosens policy prematurely," Singapore-based QCP Capital said in its 2023 market unwrap note.

"Fears of the same double-dip inflation as the 1970-80s is deeply edged in the FOMC's psyche," QCP said.

In other words, the Fed, being aware of the premature liquidity easing of 1975 and the subsequent sharp rebound in inflation, is unlikely to give up tightening and pivot in favor of rate cuts anytime soon. That would keep potential gains in risk assets in check.

QCP expects large rallies to be met with strong selling pressure and prefers writing or selling bitcoin call options or bullish bets at a $20,000 strike price.

Bitcoin changed hands at $16,850 at press time.

Related news

Bitcoin Climbs 3% to Retake $68K With Solana Outperforming, Ether Showing Relative Weakness

Bitcoin ETFs Will Soon Hold 1M Tokens, Nearly as Much as Satoshi

As 'Sentient Memecoins' Become Latest Crypto Fad, GOAT Surges to $800M and an AI Rambles

First Mover Americas: BTC Rebounds to $67K After Subdued U.S. Economic Data Reading

Solana Looks Overbought Against Ethereum; BTC-Gold Ratio Stuck in a Downtrend