Gemini’s Bitcoin Inflows From Other Exchanges Dropped to Roughly Six-Year Low, CryptoQuant Data Shows

Executives at Gemini, the crypto exchange led by Cameron and Tyler Winklevoss, have insisted in a blog post that the halt in customer withdrawals on the company’s $900 million Earn program “does not impact any other Gemini products and services.”

But a close look at blockchain data reveals a recent slowdown in incoming bitcoin (BTC) transfers to Gemini from accounts at other exchanges, which analysts see as a possible sign some crypto traders have become more leery of sending their assets to the main platform.

Bitcoin holders might not be making the distinction that the yield-focused Earn program is separate from the exchange.

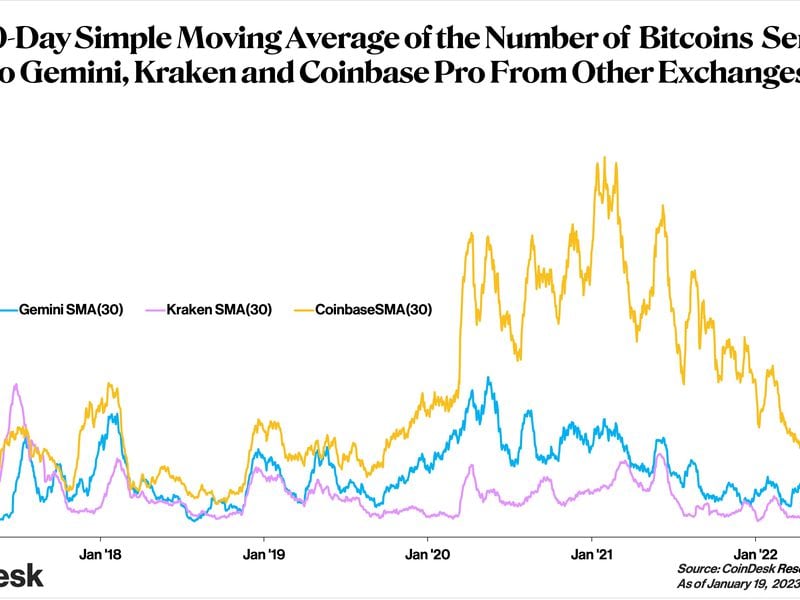

On-chain data sourced from CryptoQuant shows that the 30-day simple moving average (SMA) of BTC inflows to Gemini has ranged between roughly 100 BTC and 200 BTC in so far in 2023, down from roughly 1,100 BTC to 2,300 BTC about six months ago. The average dropped to 106.5 BTC on Jan. 8, the lowest in almost six years.

“Declining BTC inflows from other exchanges to any particular exchange could suggest investors/traders see that particular exchange as less desirable to have their coins on,” said CryptoQuant in a report on Jan. 3.

The overall industry has been hit hard in this bleak crypto winter, and yet other crypto exchanges have not seen such a dramatic fall in their BTC inflows as Gemini.

For example, Kraken’s and Coinbase’s current 30-day SMAs for their BTC inflows are not close to their six-year low. In 2023, Kraken’s incoming BTC transfers have oscillated between roughly 700 BTC and 1,030 BTC, while Coinbase’s have ranged from roughly 2,800 BTC to 3,700 BTC. Kraken and Coinbase BTC inflows have grown 42.5% and 30.5, respectively, this month, according to CryptoQuant.

Controversy over Gemini’s Earn program

Gemini executives have blamed the withdrawal halt at the Earn program on a separate withdrawal halt at the crypto trading and lending firm Genesis, a unit of the blockchain conglomerate Digital Currency Group (which also owns CoinDesk). Under the terms of Earn, customers would earn yield on their deposits. Gemini, in turn, transferred the deposits to Genesis, which promised to invest those deposits for interest.

But when Genesis fell on financial difficulties it halted withdrawals, forcing Gemini to impose the halt on its own clients.

Not only has the matter erupted into a feud on Twitter between Cameron Winklevoss and Barry Silbert, the DCG CEO, but the failed business arrangement also has now prompted a lawsuit by the U.S. Securities and Exchange Commission.

Walter Teng, vice president of digital asset strategy at Fundstrat Global Advisors, said the inability for users to withdraw from Gemini’s Earn program has “negatively” affected people’s perception about Gemini.

“The $900 million hole exists because they trusted DCG to begin with, and I think the markets are sort of realizing that and reacting accordingly,” Teng said. “If customers previously lent to Gemini 10%, who then lent out to this lending desk conglomerate, who then lent out to degen trading firms, it’s just tough to be rest assured.”

In response to a request for comment from CoinDesk, Gemini’s head of communication, Natalie Rix, highlighted the website for the Gemini Trust Center, which states that “Gemini is a full-reserve exchange and custodian. This means that all customer funds held on Gemini are held 1:1 and available for withdrawal at any time.”

Gemini did not respond to a follow-up question that focused on the decline of BTC inflows from accounts on other exchanges.

Related news

Three Arrows Capital Founders Launch Exchange Where You Can Trade 3AC Bankruptcy Claims

Bitcoin Miners Surface for Air as Sliding Natural Gas Price Provides Cost Relief

FanDuel Co-Founders Raise $4M for Digital Music Collectible Startup Vault

Bank of America: Innovation to Expand Decentralized Finance Functionality Over Time

Bitcoin Exchange LocalBitcoins to Close, Citing Market Conditions