Crypto Long & Short: Bitcoin's Hedge Potential

Greetings. I’m Glenn C. Williams Jr., and it's my pleasure to join as author of this newsletter.

I come from traditional finance, where I covered the oil-and-gas sector as an analyst. My transition to digital assets has been informative and enjoyable. Because many readers here are sophisticated, I want to provide data that could lead to profitable cryptocurrency decisions.

Here are the pillars of my research-and-analysis process:

- Macroeconomics

- Price action

- On-chain analytics

- Regulatory concerns

- Dynamics of the asset itself (supply, use cases, etc).

I also want this to be a two-way conversation, so please reach out to me with your comments and questions.

Bitcoin Failed as an Inflation Hedge. But It Was Nonetheless a Hedge

You need not look hard to find people calling bitcoin (BTC) a hedge against inflation, something that should rise in price if inflation is high. For years, that was a common refrain, and it still is in some places. And yet the past year suggests that's not true. Bitcoin has lost more than two-thirds of its value amid the toughest bout of inflation in four decades. Some hedge.

But I think bitcoin was a hedge against something else: inept central bank policy. It’s a seed of an idea that Renzo Anfossi, a senior trader at Arca Funds, planted in my head during a conversation recently – and I believe it explains a lot.

Federal Reserve officials spent months in 2021 saying red-hot inflation would prove transitory. Chairman Jerome Powell didn’t change course until November of that year, when he backed away from calling it a passing phenomenon. Bitcoin skyrocketed up until that point as policymakers appeared to be in denial.

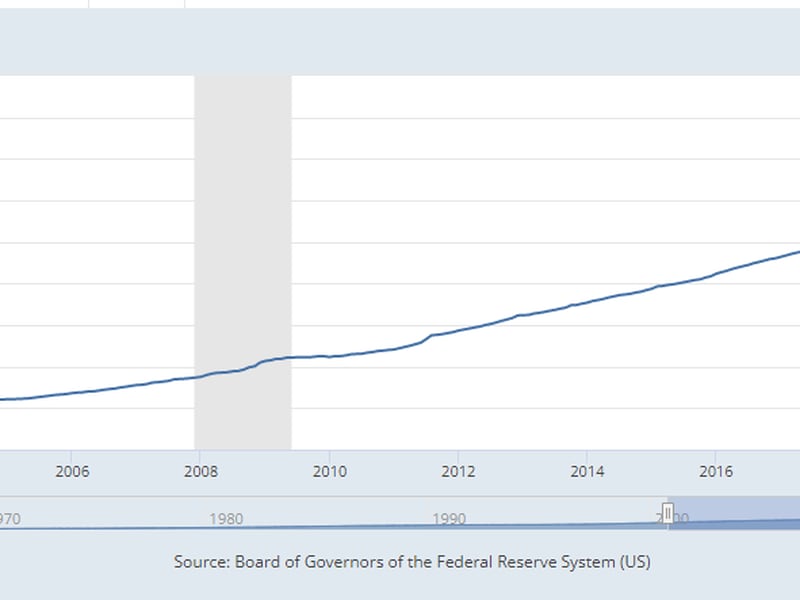

The Federal Reserve poured money into the financial system to prop it up during the pandemic. M2, a measure of the money supply, jumped dramatically from about $15.5 trillion in March 2020 to a peak last year of $22 trillion. The Fed also knocked its main policy rate target down to zero. Dumping all this cash into the system and engaging in unconstrained monetary policy encouraged questionable risk-taking in markets. Bitcoin’s rise was a clear barometer that something irresponsible was going on.

Then bitcoin crashed. It is not, I would argue, a surprise that this largely coincided with the Fed starting to raise rates a year ago – aka getting more responsible. Now, the end of Fed rate hikes to suppress inflation appears to be in sight. The central bank's target rate is now 4.5%, and policymakers have suggested 5% or so will mark the end of their campaign. M2 has fallen some, slipping to almost $21 trillion. The yield curve comparing two-year and 10-year Treasurys remains inverted at about minus 69 basis points, but that's an improvement from minus 84 basis points in early December – a sign of movement toward a more normal economy.

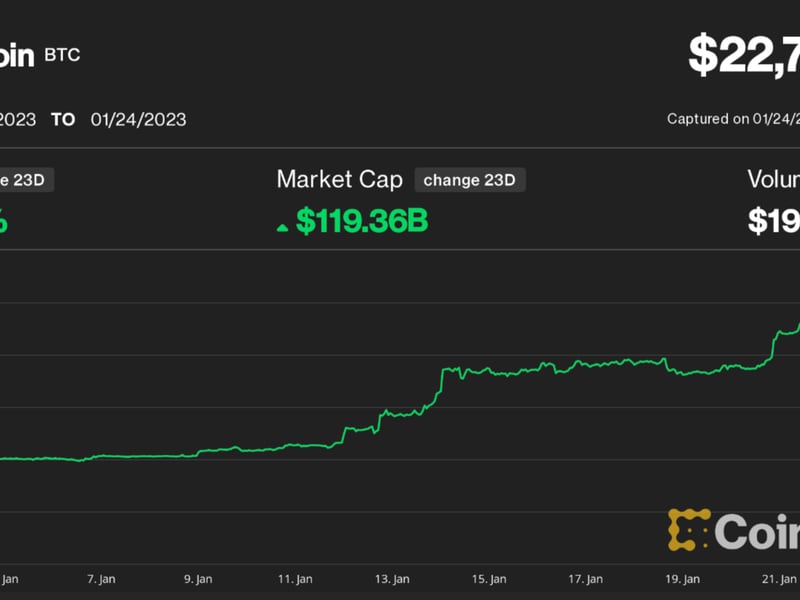

Bitcoin has soared early this year, surpassing $23,000 after being below $17,000 as recently as Jan. 8. Is that a sign of more central bank ineptitude? Not in the U.S., where it seems inflation is getting under control as the easy-money days appear to be far in the past.

What I think is happening is we're entering a period where bitcoin trades on multiple narratives. In the U.S., it’s being viewed as a tool for speculation and something valued for the technology that undergirds it.

Elsewhere in the world, ineptitude could remain a driving force for bitcoin investors. The Chainanalysis 2022 Geography of Cryptocurrency report highlights bitcoin adoption rates around the globe. Not surprisingly, a number of countries that are using bitcoin the most are saddled with numerous issues specific to monetary policy. Venezuela and Argentina, which have key interest rates above 60% and inflation near or above 100%, stand out in particular.

The U.S.-style speculative approach and central bank ineptitude angle seen elsewhere can both be bullish for bitcoin. Things have been considerably bullish in crypto recently, and not just for bitcoin. Bitcoin is up 37% this year and ether (ETH) is up 36%.

How bitcoin ultimately behaves as an asset is yet to be seen. It remains relatively young, and opinions vary by the audience. The goal of “Crypto Long & Short” will be to highlight those views, so that they can be acted upon.

Crypto Diversification Is Back in 2023

Throughout 2022, cryptocurrencies and stocks – specifically growth tech stocks – moved more in lockstep than they did in 2020-2021. That can be explained by similar, shared investor types and overlapping investment views that called for positioning toward future technology adoption despite the risk of uncertain and unpredictable future cash flows.

Whatever the case, the dramatic rise in interest rates in 2022 had a meaningful impact on growth-oriented portfolios. Investors’ time horizons collapsed from more than five years out to the near term. Today, investors are making current cash flows and profits a priority over potential growth prospects. Bull market buzzwords – fear of missing out, moon bags, laser eyes, stonks go up, and financial independence, retire early – are out of vogue, replaced by mundane things like holding on, dollar cost averaging and the collective hope for transitory inflation.

With this sudden change in mentality gripping crypto investors unaccustomed to inflation or a persistent bear market, crypto started trading interchangeably with other risky assets. (See rolling correlations to key exchange-traded funds in Figure 1):

Fortunately, crypto and other assets are going their own way in 2023, with the bitcoin/Nasdaq (QQQ) correlation down to levels last seen in 2021. Correlations to gold (as represented by the GLD ETF) and bonds (the TLT ETF) have slipped back to around zero, meaning no real relationship. Diversification is back.

A useful analogy for correlation changing under market stress would be to imagine yourself standing outside your house when it’s on fire. Amid shock and disbelief, you lose any semblance of nuance or long-term perspective. The only thing that matters is who’s inside the house and who’s safe outside. Few people ever plan for these circumstances, and for those who do, as Mike Tyson famously said, “Everybody has a plan until they get punched in the face.”

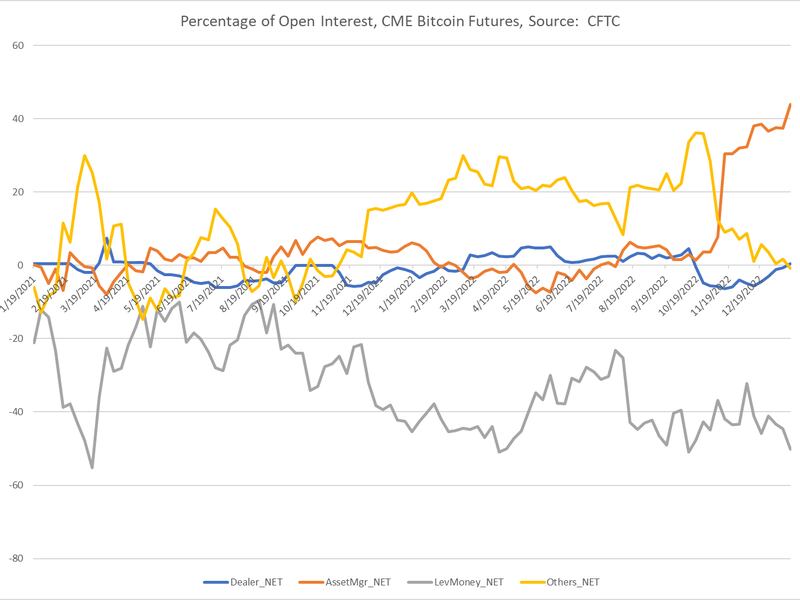

Only once the flames subside can we begin to make calm and reasoned decisions. That’s happening now as crypto prices surge. My inner contrarian initially wrote off this move higher as a bear market short squeeze, but futures positioning data from the Commodity Futures Trading Commission (see Figure 2) tells a different story. Over the past three weeks, there has been an uptick in open interest from the real-money crowd (i.e., asset managers), while the fast-money crowd (“leveraged funds” in CFTC parlance) doesn’t appear to be overstretched and therefore vulnerable to a short squeeze. That suggests the rally is durable.

- Todd Groth, CFA; head of research at CoinDesk Indices

Takeaways

Here’s some news you should know about:

- APTOS’ APTITUDE: The crypto rally is far from limited to the BTCs and ETHs of the cryptosphere. A terrific example of that is the huge jump in the APT token from Aptos, the vaunted Solana-killer (which was itself been pitched as an Ethereum-killer), as well as the increased interest in the shiba inu token (SHIB). Who knows if that’s sustainable, but risk is being sought in more far-flung corners of crypto.

- YES, BUT WHEN?: Pantera Capital, a crypto investment and venture-capital firm with about $3.8 billion of assets under management, is looking toward the future, writing recently that it sees the business of finance moving over to blockchain infrastructure. It’s an old idea at this point with, frankly, not much real progress, but Pantera isn’t the only player still confident it’ll happen eventually. Hopes that traditional finance and crypto will intersect remain eternal.

- MORE WAITING: Here’s another immortal idea: Crypto regulation is coming. There’s no question FTX’s collapse adds urgency to a topic that’s been talked about and talked about and talked about. Don’t forget, though, that a CoinDesk deep dive showed one in three members of the U.S. Congress have received money from FTX officials like Sam Bankman-Fried, creating awkwardness amid any regulatory push.

- JUST ANOTHER DAY: Crypto lender Genesis (CoinDesk’s corporate sibling) recently fell into bankruptcy court. An on-chain analysis reveals, though, that the separate Genesis trading division is showing some semblance of normalcy. On the same day the crypto-lending arm began Chapter 11 proceedings, the trading business moved a lot of ETH around. It was one of its busiest days ever, in fact.

Related news

Three Arrows Capital Founders Launch Exchange Where You Can Trade 3AC Bankruptcy Claims

Bitcoin Miners Surface for Air as Sliding Natural Gas Price Provides Cost Relief

FanDuel Co-Founders Raise $4M for Digital Music Collectible Startup Vault

Bank of America: Innovation to Expand Decentralized Finance Functionality Over Time

Bitcoin Exchange LocalBitcoins to Close, Citing Market Conditions