What’s Inside the FSOC’s Long-awaited Report on Crypto Regulation

The Financial Stability Oversight Council (FSOC) published its own highly anticipated report in response to U.S. President Joe Biden’s executive order on crypto earlier this week, calling on Congress to define the line between a security and a non-security, at least as far as crypto is concerned.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

FSOC: Do something, Congress!

The narrative

The Financial Stability Oversight Council (FSOC) finally published a long-anticipated report about the regulation of crypto. Essentially, FSOC said it believes federal agencies already have much of the authority they need to oversee large chunks of the crypto sector. The one area it really asked for Congress to get involved is defining just where the limits of securities regulation should be. In other words, much of this wasn’t really a surprise.

Why it matters

Where the line is between a crypto security and a crypto commodity is the question in the U.S.: Where exactly does the Securities and Exchange Commission's authority end and the Commodity Futures Trading Commission's authority begin? Congress has not really tried to answer that question. Sure, there are bills that sort of seek to address that, such as the Senate Agriculture Committee’s DCCPA. But a closer look at the text shows that it doesn't actually provide that definition. This has left much of crypto in an odd sort of limbo.

Breaking it down

FSOC published a 124-page document on Monday. Here’s CoinDesk’s Jesse Hamilton on the highlights.

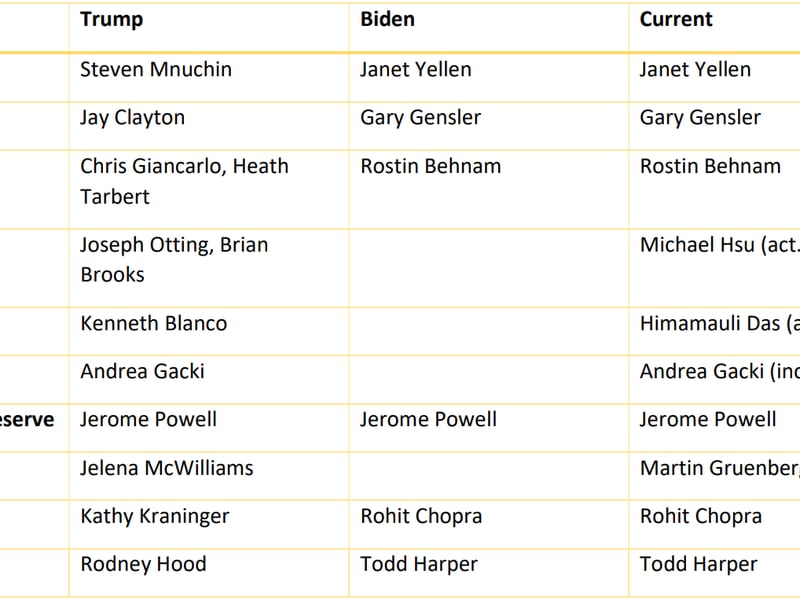

As a quick reminder, the council is composed of Treasury Secretary Janet Yellen, Federal Reserve Board Chair Jerome Powell, Acting Comptroller of the Currency Michael Hsu, Consumer Financial Protection Bureau Director Rohit Chopra, Securities and Exchange Commission Chair Gary Gensler, Commodity Futures Trading Commission Chair Rostin Behnam, Federal Deposit Insurance Corporation Acting Chair Martin Gruenberg, National Credit Union Administration Chair Todd Harper and a handful of others.

The actual report went largely into detail on what currently exists in crypto, detailing existing rules and regulations, some of the recent events and precedents that we’ve seen and a summary of how regulators see crypto posing eventual risks to the U.S. and possibly the broader financial system.

“Some characteristics of crypto-asset activities have acutely amplified instability within the crypto-asset ecosystem. Many crypto-asset activities lack basic risk controls to protect against run risk or to help ensure that leverage is not excessive. Crypto-asset prices appear to be primarily driven by speculation rather than grounded in current fundamental economic use cases, and prices have repeatedly recorded significant and broad declines,” the report said.

The report also took aim at how a lot of the companies that offer services in the crypto ecosystem advertise themselves as regulated. They’re not lying, but the report is concerned that usually this means they’re overseen as money transmitters.

FSOC is concerned that money transmitter frameworks don’t have a huge focus on anti-money laundering controls, customer protection and absolutely does not look at financial stability concerns.

In particular, the report says that there are issues with the spot market for cryptocurrencies. Namely, there is no federal spot market regulator or framework. There's also no real international framework, which could allow different entities to conduct regulatory arbitrage.

Another concern seems to take aim at FTX (and I guess CME now) by noting that some platforms want to offer retail customers direct access to their markets, which again raises some stability questions.

In short: Financial stability (obviously) is the key concern by way of how crypto interacts with the rest of the world, whether that’s through stablecoin payments, banking activities, tokenized real-world assets, investment products or even just this general idea that crypto and crypto tools may be used to facilitate, replace or even just bolster some of the more traditional financial activities that take place out there.

And then there's the hacks and crashes. A fairly significant section of the report is focused on the fact that much of crypto is built around speculative trading, but is vulnerable to frequent hacks (as of this writing, the most recent hack is around 15 hours old) and other issues.

“Fundamental economic use cases do not currently anchor prices of many crypto assets. Rather than reflecting analysis of cash flows, crypto-asset prices may reflect the probability that economic use cases could develop in the future, balanced against the probability, as expressed by some industry commenters, that no significant economic uses for blockchain technologies may develop,” the report said.

The prevalence of (alleged) fraudsters also naturally takes on a star role.

To wit: The important part is the recommendations here. The first two are straight forward –= regulators should treat crypto risks like they treat other risks, keep enforcing rules, etc.

The third, fifth, sixth recommendation calls on Congress to get busy.

“The Council recommends that Congress pass legislation that provides for explicit rulemaking authority for federal financial regulators over the spot market for crypto-assets that are not securities,” the report said in recommendation three. “The Council recommends that this rulemaking authority should not interfere with or weaken market regulators’ current jurisdictional remits.”

Recommendation five called for stablecoin legislation, six called for letting regulators coordinate or even supersede affiliate and subsidiary regulation (if those subsidiaries are operating under, say, a state regulator rather than a federal one),

Other recommendations include closer coordination between different regulators, whether that’s state-to-state or with different types of regulatory entities, and having federal regulators continually build out and reassess their crypto knowledge as they oversee and license different entities.

There's also a call for “a coordinated government-wide approach to data and to the analysis, monitoring, supervision, and regulation of crypto-asset activities. The Council recommends that member agencies consider the use of available data collection powers in order to facilitate assessments of the financial risks related to crypto-assets, as part of data sharing and coordination efforts among the members.”

The other thing that’s really interesting is we sort of previewed the report on Monday with the New York Fed, which published a research paper earlier in the day detailing some of the concerns that exist about stablecoins. In particular, it said even supposedly safe stablecoins like USDC might pose a risk to the broader financial sector if it becomes a safe haven for people fleeing less-safe stablecoins backed by sketchy assets.

Biden’s rule

Changing of the guard

N/A

Elsewhere:

- Italy Hasn't Vetted the 73 Crypto Firms It Approved This Year: Italy’s approved 73 crypto firms to operate this year. What the country’s financial supervisor hasn’t done is vet these companies, or check if they actually have offices in the country. Sandali Handagama takes a look at this frankly questionable state of affairs.

Outside CoinDesk:

- (Unchained Podcast) I don’t normally share stuff I’m on but I had a fun conversation with Laura Shin on her “Unchained” podcast about the CFTC v. Ooki DAO suit, and the different peculiarities it presents.

- (Wall Street Journal) I’m not great at economics but this seems worth flagging: Cargo shipping entities are planning for reduced demand.

To be fair, Google Stadia faced terrible odds in the past 3 years, having to deal with:

— Aadit Doshi (@AaditDoshi) September 29, 2022

- a global pandemic forcing people to turn to online entertainment.

- graphic cards and console shortages, creating high demand for alternatives.

If only they hit the market at a better time

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at [email protected] or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!

Related news

Jebara Igbara, AKA 'Jay Mazini,' Sentenced to 7 Years in Prison for Crypto-Related Fraud

Stablecoin Bill Could be Ready for the U.S. House Soon Says Top Democrat Maxine Waters: Bloomberg

Samourai Wallet Founders Arrested and Charged With Money Laundering

Binance Founder Changpeng Zhao Apologizes Ahead of Sentencing, 161 Others Send Letters of Support

Nigeria Directs Entities to Identify Those Dealing Crypto With Bybit, KuCoin, OKX and Binance